A well-researched study

First of all, the Citi GPS study is very well researched and written. Gone are the times of Bitcoin being called “fraud” or “rat poison squared” by major banks’ CEOs and celebrity investors. Citi’s report was written by a team of six professionals that know their subject matter. Moreover, the team consulted with some of the industry’s foremost players, such as Nick Carmi from BitGo and Zac Prince from BlockFi.

Bitcoin at the Tipping Point works as a great introduction to Bitcoin in general. It explains Bitcoin’s cypherpunk origins, Satoshi Nakamoto’s design decisions, and major historic milestones. It spells the importance that censorship resistance and permissionless transactions played in Bitcoin’s early adoption among libertarians, hackers, and yes – even some criminal elements. The study also points out that today, less than 0.5% of Bitcoin transactions can be characterized as illicit. And most of all, the report analyzes why Bitcoin is important and willful ignorance and dismissiveness come at a cost to their holder.

Bitcoin becoming an institutional play

In the early years up to circa 2016, Bitcoin was mostly popular among the fringe groups and risk-prone traders. In the 2017-2018 speculative bubble, a mass of retail investors discovered Bitcoin and cryptocurrencies, namely due to the emergence of accessible crypto exchanges. And in the past few years, the industry underwent another giant leap, finally enabling institutions to come in.

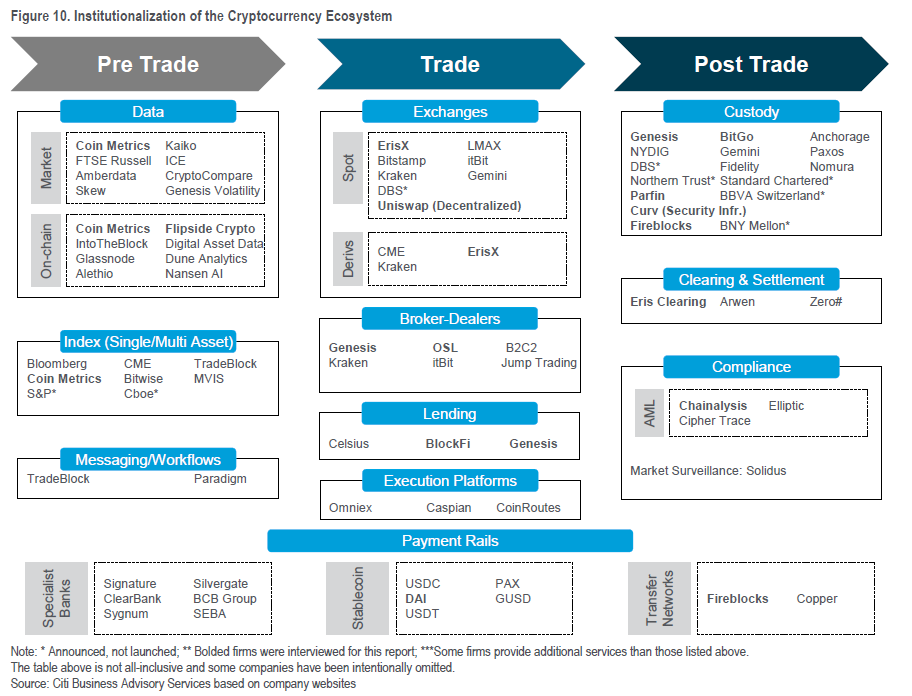

“For institutional investors to participate in a new asset class, it must be underpinned by a robust infrastructure able to support an efficient market,“ write the authors regarding the gradual institutionalization of the Bitcoin ecosystem. This robust infrastructure is mostly characterized by the professionalization of three fields:

1) Data – there are two distinct groups of data within Bitcoin: market data and on-chain data. Market data access and analysis has expanded in recent years thanks to specialized analytics companies such as Coin Metrics, as well as reliable exchange APIs. On-chain data metrics and analytics also underwent a leap forward in recent years – a development partially motivated by a growing need to economize on ever-growing on-chain transaction fees.

2) Exchange and Trade offerings – In recent years, exchanges began to utilize FIX protocols (widely used in conventional finance infrastructure). New exchanges are nothing like buggy and hackable early exchanges. Derivatives offered by Chicago Mercantile Exchange (CME), Bakkt, and others are growing in volume and open interest, providing institutional players with well-known instruments such as futures and options contracts. Many institutional investors utilize Grayscale’s Bitcoin Trust (GBTC), the AUM of which has grown from $2 billion in December 2019 to $36 billion in April 2021.

3) Custody – safekeeping with qualified custodians is often a regulatory requirement for the institutions to acquire assets such as Bitcoin. The emergence of professional custody providers BitGo, Anchorage, or Unchained Capital has partially resolved the issue that has been preventing institutional entrance for years. But the largest game-changer was the entry of traditional custodians – Northern Trust, Bank of New York Mellon, Nomura, Standard Chartered, BBVA, and DBS have all launched institutional crypto custody solutions in 2020-2021.

Another major obstacle for institutional adoption was regulatory uncertainty. This has also changed in the past three years, and various rulings and statements on Bitcoin and other cryptocurrencies made a lot of things clearer. Specifically for banks, the U.S. Office of the Comptroller of the Currency (OCC) Interpretive Letter on Banks Using Blockchain Networks for Payments is an important milestone, as it enables banks to use blockchain applications and stablecoins.

As for the question of who the institutional investors are, the authors give the following answer:

“Two types of institutional investors are entering the market. Those looking to profit from market inefficiencies are helping to narrow the price volatility and provide more consistent liquidity and those with deep pockets that are bringing large sums of capital into the market, adding support to price dips as they build positions for a long-term strategies.”

The first type of investor is seldom talked about, though very necessary for market maturation. The second type – “hodlers” such as MicroStrategy or Tesla, got the most spotlight in the past year, as these reinforce Bitcoin’s store of value narrative.

Store of value is an important monetary function – one which fiat money is gradually losing due to unprecedented monetary policies. But, as the Citi authors argue, Bitcoin can very well start fulfilling another monetary function: an international medium of exchange.

Bitcoin as a potential global trade facilitator

Source: Bitcoin at the Tipping Point, p.5.

There is potential that in the future perceptions about Bitcoin might end up focusing on its global reach and neutrality.

Bitcoin at the Tipping Point, p.83.

The Citi GPS report culminates with the main theme of Bitcoin potentially becoming a global trade facilitator. As shown in the picture above, the perceptions concerning Bitcoin have evolved over the years from the new type of payment system to an internet-native currency, a digital gold, and finally to a possible global value exchange network.

The authors offer the following supporting arguments for the potential perception shift:

1) Borderless design. No government controls Bitcoin; this neutrality can prove as a killer feature in a world of increasing west-east tensions. Bitcoin can become a universal settlement currency for cross-border contracts and transactions, especially in countries with high domestic currency volatility.

2) Lack of FX exposures. Gone may be the days of multi-currency trade deals with exchange rate risks if Bitcoin is adopted as a universal settlement currency for multiparty deals.

3) Faster, potentially cheaper money movements. Settlement in the Bitcoin network takes around 10 minutes when a sufficient transaction fee is paid. While on-chain transaction fees may be too high for smaller payments, it is quite negligible for payments of several thousand dollars and more, especially when the final settlement takes such a short time. And Bitcoin’s Lightning Network offers instant, near-costless payments on top of that (mostly for smaller payments).

4) Secured payment. Bitcoin carries no risk of chargebacks or payment bouncing. The entity sending bitcoin has to have the money to be able to initiate the transaction, and when first network confirmations appear, it is impossible to revert the transaction.

5) Traceability. Bitcoin transactions are transparent and trackable on the blockchain, full consequences of which are still to be discovered. The study’s authors point out that smart payments can be built on top of transparent Bitcoin transactions, i.e. automatic payments conditional on previous payments, the flow of goods, etc.

While this vision is highly optimistic about Bitcoin’s future potential, the authors concede there are obstacles on the way. Capital efficiency, insurance and custody concerns, security concerns, or energy consumption worries are cited.

Bitcoin at the tipping point

In conclusion, the authors remark that Bitcoin went from a ridiculed niche concept into a leader of a huge, growing industry, where even central banks are considering following the example and launching their own Central Bank Digital Currencies (CBDCs – we’ll cover them in the future blogpost). Bitcoin made this leap in little more than a decade since its inception. In this context, imagining a future where Bitcoin plays a major role in world trade doesn’t seem so far-fetched.

But Bitcoin being “at the tipping point” implies that it may also not make the final move over the crest. According to the Citi GPS team, Bitcoin has two possible futures: mainstream adoption, or speculative implosion. The implosion may come as a combined result of a shift in the macro investing environment (due to tapering of the loose monetary policies) and regulatory oversight chasing away the most promising Bitcoin developers and entrepreneurs.

The idea that Bitcoin will either go mainstream or die is actually nothing new. In 2010, Satoshi Nakamoto said:

“I’m sure that in 20 years there will either be very large transaction volume or no volume.”

So far, the transaction volume has been growing at an increasing pace. And the big players like Citi are taking the notice.

The Bitcoin network is the first truly global payment system. It knows no borders, never closes, is not owned by anyone, and is accessible to everyone. Unlike traditional payment systems that exist on private servers, the Bitcoin blockchain is distributed across thousands of machines all over the world. Anyone can maintain their own copy of the shared ledger.

Bitcoin at the Tipping Point, p.17.