Niche banks are on the rise and continue to form an important part of the new wave of neo-banks. In our previous article, we explored a few of these banks and how they are deeply tailored to fulfil the needs of their target customers in the consumer space.

In this article, we will explore the potential of niche banks in the SME and Corporate spaces and whey they can have a huge impact.

First, let’s take a brief look at traditional customer segmentation and disruption in financial services. Banking has typically been characterized by a few broad customer segments:

- Individual (mass, affluent, high net worth)

- SME

- Corporate

Second, let’s think about the disruption in financial services. It has historically tended to start with the consumer segment, and then permeate upstream into the SME and Corporate spaces.

The nature of segmentation and manner in which digital disruption occurs makes the SME and Corporate segments ready for disruption from niche banks. Furthermore, potential new entrants in this space are at an advantage as they can look to what success and failures of niche bank disruptors in the individual space.

Current state of play

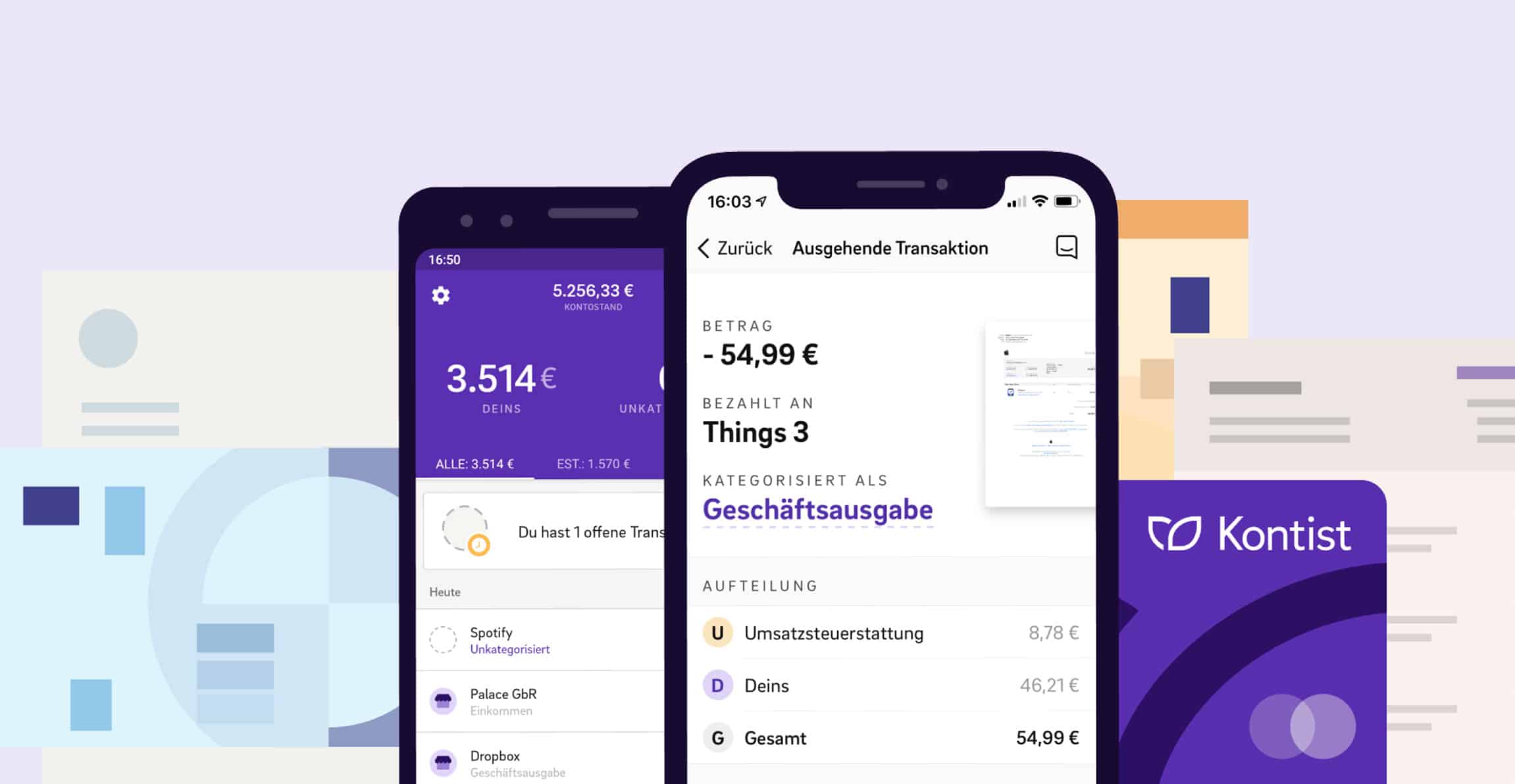

The current wave of niche SME neo-banks is largely focused on the type of business, rather than the industry in which the business operates. For example, Kontist and Coconut are two examples of niche banks catering to the solopreneur and freelance segment respectively. This has created a nice starting point for the next wave of disruptors.

The Corporate space, however, is yet to experience a holistic neo-bank revolution. Instead, we are seeing a range of fintechs and vendors that are supporting the various players of the Corporate banking value chain (e.g. Kantox) for the leading global banks and also high levels of cross-bank collaboration (e.g. R3), specifically in the blockchain space.

We see two primary ways in which niche banks can evolve and compete in the SME and Corporate segments. Within the SME space, new niche banks can focus on incorporating value-added services in addition to core banking products based on the sector in which the business operates.

Moving up to the Corporate segment, we envisage something more disruptive. Will large corporates start partnering with banking-as-a-service (BaaS) and other tech-first companies at an ever-greater pace to create financial products and services to achieve greater customer lifetime value?

Barbershop, Blockchain and Bakery: The secret sauce to the SME niche bank

What Coconut, Penta and Kontist (amongst others) have done for the respective customer segments has really set the ball rolling for innovations within the SME world. Creating bank accounts that are tailored to how the business operates, rather than solely based on turnover, has certainly saved many hours for business hours in their respective markets.

We see the next wave of offerings in the SME space going one step further, and catering to specific industries. We are beginning to see such offerings – Squire and its play into the Barber Shop space serves here as a great case in point.

Squire is a Y-combinator backed business management platform for barbershops, operating in 28 cities in the US and processing more than $100 million in transactions since 2016. It positions itself as an all-in-one platform to power barbershop operations, offering:

- A CRM system

- Marketing platform

- Payroll management

- E-commerce

- Appointment scheduling

- POS solutions

Squire is not a bank, nor does it offer any core banking products and or services besides the POS capability. However, Squire could easily partner with an existing bank or utilize a BaaS provider with a license to begin offering business current accounts or specialize in lending for barbershops looking to expand their operations. Alternatively, a new bank looking to carve out a niche in the personal grooming space could easily partner with Squire to complement its core banking services with non-core banking services to truly be the one-stop-shop for barbershop owners.

While Squire is targeting industries with physical operations, there is one sector in the tech space that has received quite a bit of attention in terms of niche offerings from banks. We are beginning to see the development of niche banks also in the cryptocurrency and blockchain industries largely from established tech-first banks. Solaris Bank and Fidor Bank, two BaaS providers, have created specialized services for businesses in the blockchain and cryptocurrency spaces aimed at businesses on the medium to the larger end of the business spectrum.

The Solaris Blockchain Factory offers a Pooling Account Solution, that tackles the issues cryptocurrency exchanges or marketplaces are faced when it comes to custodial, AML and fiat to crypto on and off-ramping. Fidor Bank offers it’s Crypto As a Service, offering a specific solution for those companies looking to ICO in addition to Exchange Accounts. One to watch is Founders Bank Project, an early stage Malta-based startup that is looking to set up a corporate challenger bank for companies in the blockchain, crypto and tech industries.

The barbershop, cryptocurrency and blockchain industries are a handful of industries in which niche banks can successfully operate. The secret sauce here is to integrate non-core banking products and services into a holistic platform to truly be part of the end to end customer lifestyle while localizing on a particular market or region.

For example, Germany is ranked the 5th largest bakery market in the world and is the largest in the European Union (EU). A niche bank can take a look at this segment and create a bank based on the core financial needs of bakeries (of course segmenting between small, medium and large) and incorporating non-core banking services such as specific inventory tools, digital tools and platforms for banking courses, loyalty and so on.

[related_article]

Large Corporates: The next neo-banks?

So far we have discussed the potential for our traditional view of a bank to become a niche bank. However, as we travel further up the business spectrum to the larger corporates, we see greater scope for businesses to offer financial services themselves. Bringing financial services in-house can be achieved via strategic partnerships.

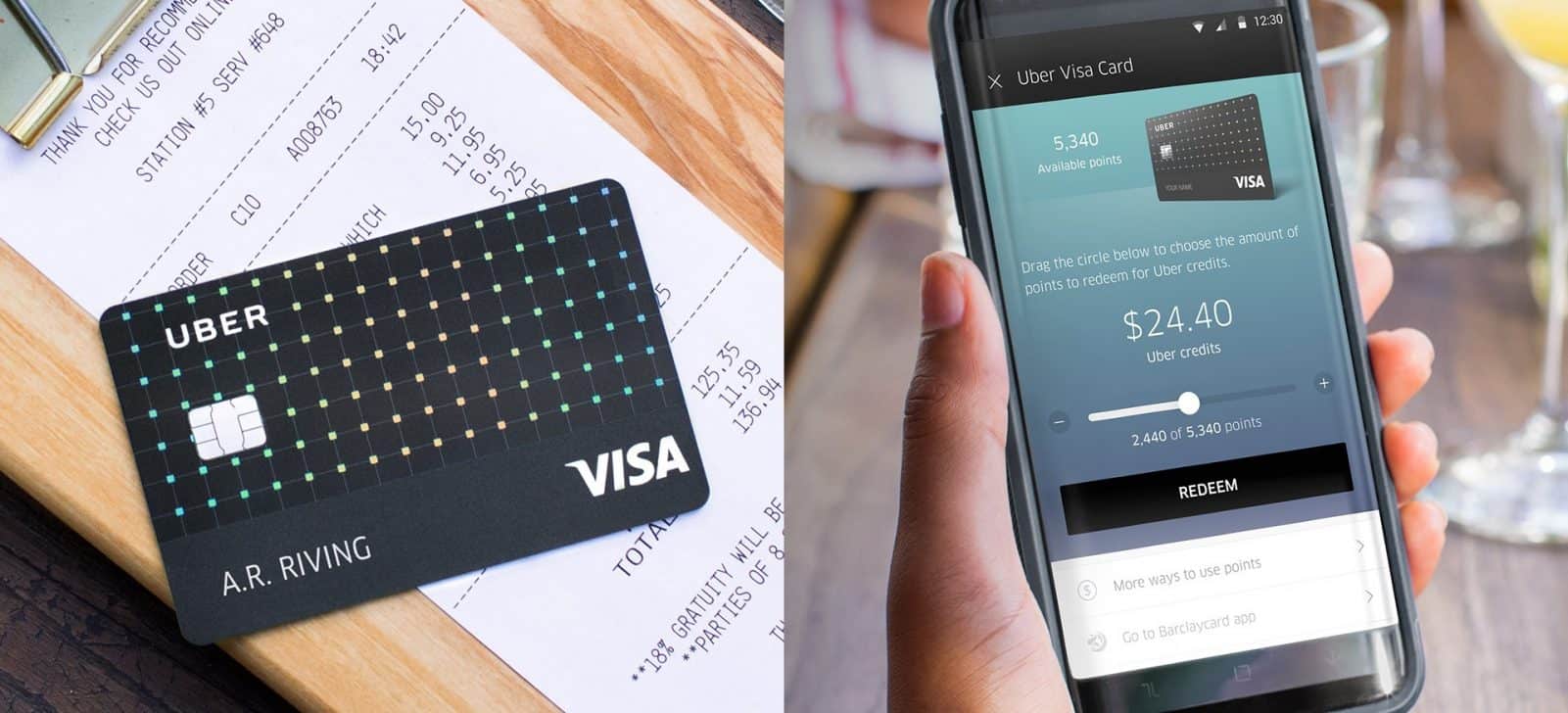

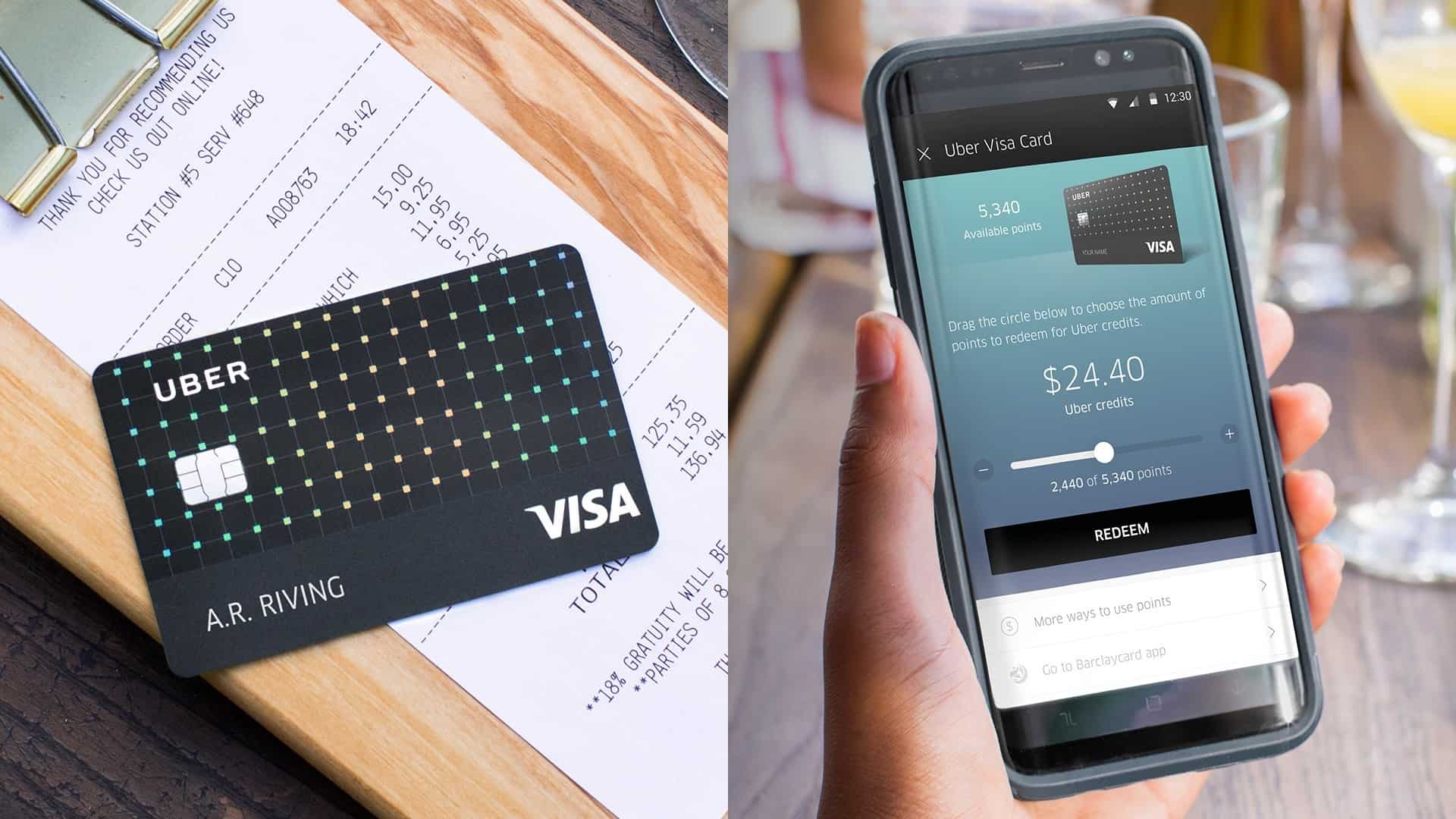

Perhaps one of the most known examples is the partnership between Uber and GoBank in the US. The Uber Checking account by GoBank provides tailored services to Uber drivers, such as 2x cash back at gas stations and auto-care companies. For example, drivers can receive a 3% Cash Back at Exxonmobil and a 15% discount on select services at Jiffy Lube, an auto-care company. The bank account is promoted to drivers when they sign up to become an Uber driver. Another feature specific to Uber drivers is the ability to “cash-out” up to 5 times per day for free.

Aside from the Uber Checking account, there is a huge potential for Uber to offer financial products and services to its lesser-known segments. For example, Uber for Business has created a suite of products revolving around its business customer needs. It offers:

- Employee travel management solutions

- Easy integrations for travel expenses

- Courtesy rides as a way to increase loyalty

- Shuttle programs for events

Uber is in a prime position to partner with a bank or offers its own services to provide a one-stop-shop for travel management and banking. We wouldn’t expect Uber to become the primary bank for its business and corporate customers, but it could create a unique unbundled offering in corporate expense, payment reconciliation and even corporate card space.

Large corporates in the luxury goods sector could also take financial services in house, specifically as a means for increasing customer loyalty. This could coincide with the rise of metal-like cards we are seeing in the consumer space. Consumers loyal to the likes of Louis Vuitton, Bentley, or W-Hotels could see cards, perks or perhaps investment products that play to their brand loyalty and desire for exclusivity.

Imagine a gold plated credit card offered by Louis Vuitton for customers spending a certain amount per year, or exclusive investment opportunities into mobility initiatives for Bentley car owners. These plays are becoming increasingly easy with the rise of BaaS providers and fintechs.

Endless opportunities

The SME and Corporate segments are ripe for the emergence of niche banks, with the groundwork being laid by the first wave of neo-banks such as Kontist or Coconut and strategic banking partnerships by a few large tech companies.

As we discussed in the previous articles, we expect to see individuals begin selecting banking and financial products that are truly tailored to their needs, beliefs or culture. There is no reason why an SME cannot avail of the same, or why large corporates can’t morph into niche banks themselves.

A range of factors, such as the growth of BaaS providers and fintechs, the digitization of virtually every aspect of maintaining a business, and the rise of personalized services, all provide ample opportunity.

Similar to the Personal segment, the key to success is putting the day to day requirements of your business first when developing your niche bank. In this segment, there is immense opportunity to create a bank that offers core banking, industry-specific banking needs and complementary business services that fulfil the day to day requirements of running a business. With PSD2, growing partnerships, and a market full of innovation, the possibilities are endless to truly delight customers.

In our next articles, we will deep dive into the partners and pieces you need to consider in order to create your future niche bank or financial solution.